There was an old lady who swallowed a fly. I don't know why she swallowed a fly; perhaps she'll die.

I don't know if you know this nursery rhyme, but the fly was the least of the old lady's problems. She subsequently swallowed a spider (which wriggled and tickled and tickled inside here) to catch the fly. Then a bird (wasn't that weird), to catch the spider. A cat, dog, cow and finally a horse followed. She's dead, of course.

I can't help thinking that US monetary policy since the defeat of inflation in the 1980s bears some similarities to the behaviour to the old lady in the nursery rhyme. The Federal Reserve is charged with running policy in such a way as to keep inflation under control and the economy at full employment. But inflation is being kept at bay more by a global labour market and technological innovation than by anything the Fed is doing. The Fed doesn't have to 'do' anything very much to control consumer prices and this affects policy. Fed policy is geared towards reacting to periods of falling unemployment by ever-so-cautiously tightening (or un-loosening) monetary policy, because that 'seems the right thing to do'.

By contrast, at the first sign of economic trouble, the lack of inflation means that the Fed can go all in, cutting rates, allowing the dollar to fall and encouraging those who can to borrow more, in order to boost demand and help create the jobs that will get the economy back on an even keel. Indeed, we have been forced to re-think 'all-in' as we saw the Fed cut rates to 3% in 1993, then to 1% after the dot-com bubble burst and now almost to zero, with a huge QE programme on top.

Meanwhile, the United States' overall debt level has gone on going up. That's "OK" because 'net debt' is offset by asset price gains, and 'debt-servicing' is kept down by low rates. The periods of low rates have caused asset bubbles - sometimes in the US, more often elsewhere. But one man's bubble is another man's boom and asset price inflation is apparently less dangerous than consumer price inflation. Never mind that it represents a huge transfer of wealth from one generation to another, that it dramatically increases economic inequality or that asset prices have a nasty habit of coming back into line with the underlying trend of the economy eventually. What we are concerned with, is the unemployment rate and the only thing that could deflect the Fed's attention would be consumer - not asset - price inflation.

So having swallowed a recession in 1990, the US sent down a 3% policy spider to catch it. Then a bird in 1998. Then a cat in 2001 and a dog in 2008. On that basis, the cow comes next and then the horse, and it all goes wrong. I thought that 2008 was going to represent the last leg of what the Bank Credit Analyst terms the Great Debt Super-cycle. I was wrong. But was it the second-last, or the third-last?

The Phillips curve - a dinosaur

At the heart of this, is the fact that monetary policy-making is still dominated by the Phillips Curve. AWH Phillips established that there was a correlation between inflation and the unemployment rate in the UK, between the mid-19th and mid-20th centuries. The conclusion was that high unemployment pushes wages down, and low unemployment pushes them up, and this is what drives inflation. Sounds simple and plausible. Milton Friedman responded by introducing the concept of the NAIRU (non-accelerating inflation rate of unemployment) arguing that since the labour force is rational, you can't just pick a point on the Phillips curve where you choose a combination of unemployment and inflation. Unemployment would tend to gravitate back to NAIRU, and you could only hold it below that by accepting rising inflation and indeed, could only get inflation back down by keeping unemployment high.

I was reminded of how out-dated the Phillips curveseems when I read a post by the BBC's Economics Editor, Stephanie Flanders in which she argues that the cause of the relatively low unemployment rate the UK enjoys now, is falling wages. That fits in with the Phillips curve view of the world, except in the small detail that the causality is the wrong way round. Low wages keep unemployment down, as opposed to high unemployment driving wages down. So what is driving the wage growth down in the UK?

The world of AWH Phillips was one of a closed economy where people could move between industries, but not between countries. It works less well when labour can move pretty freely around the world and when productive capacity and employment can also move at the drop of a hat, to places where labour is cheaper, or perhaps where tax rates are lower. And the Phillips curve doesn't work at all if we can't even measure unemployment.

A global labour market makes casual measurement of one country's unemployment rate somewhat redundant. When goods-producers can shift production at a moment's notice to a more competitive location, the going wage rate is determined internationally, not as a result of a domestic Phillips curve. When people can come and go from one country to another, they drive down costs in many new industries. Coffee shops stand out. And as a piece I read last week by Paul Krugman argues, an economy where the biggest and most successful companies don't actually employ many people, you have to look at the labour market differently. Not least when the driving force deciding where they hire people is the corporate tax rate more than the wag rate. Finally, when we have seen a collapse in labour market participation rates in this cycle, we simply have no idea what even one country's real unemployment rate is. The 'underemployed' are people who aren't recorded as looking for work, but would love to work (or at least earn) more. And they will act as an anchor wage growth even as the 'official' unemployment rate falls.

The warning from all of this is that economic recovery may not drive inflation up, because I can't see what drives wage growth up in developed economies in this cycle. But while that's good, what it does, is lead to continued unbalanced monetary policy. The FOMC must know that current policy settings are dangerous, just as you would have thought the old lady would know swallowing a cat was a bit risky. But there's no CPI inflation and that means that if the US economy were to lose a bit of momentum, perhaps as a result of a falling stock market and rising mortgage rates, the Fed would be sorely tempted to re-inject some monetary accommodation - a metaphorical dog to get after the unemployment rate...

Saturday 22 June 2013

Sunday 9 June 2013

Are we really stupid enough to prefer 2006-2010 to 1995-1999?

I have spent the last week seeing investors in the US. there is a huge debate going on in markets at the moment about whether the US Federal reserve should, or will, slow down the pace at which they have been buying Treasuries, and what it might mean for markets. This note is a short update on the previous post I put on this blog - which was intended as a basic aide-memoire for anyone who wanted to understand a little about how the 1994 'bond crash' played out in financial markets. That period being a reference point for what happens when the Fed starts the process of exiting periods of extraordinarily accommodative monetary policy

The chart below shows US jobs and GDP growth through the 1990s. You can clearly see how in 1994/1995 (when the US Federal Reserve increased its target for Fed Funds from 3% to 6% in 12 months), employment growth slowed from around 350k/month to a trough of around 100k/m, and GDP growth slowed from 5% to 1%. Briefly. Now that is a pretty sharp slowdown and is the basis for arguing that the 'bond crash' represented at the very least a poor piece of policy communication on the Fed's part. Let's forget anything else going on in the world, and accept that if the Fed had either done a better job of preparing financial markets for the necessary monetary policy normalisation, or if they had tightened more slowly, the economy's path would have been smoother.

That's all fine. But what I find surprising is that even now, there is a general sense that the Fed should do everything in its power to avoid a repeat. "We remain unconvinced that the eventual tapering of the central bank's asset purchases will trigger a 1994-style bloodbath in the bond market", John Higgins of Capital Economics is quoted as saying in the Sunday Times today.

The sense that is conveyed is twofold. Firstly, that there is a risk that 'tapering' could be as bad in 2013 or 2014, as raising rates from 3% to 6% was in 1994. And secondly, that the crash was so disastrous everything that can possible be done to avoid a repeat, should be - despite what we have learnt since.

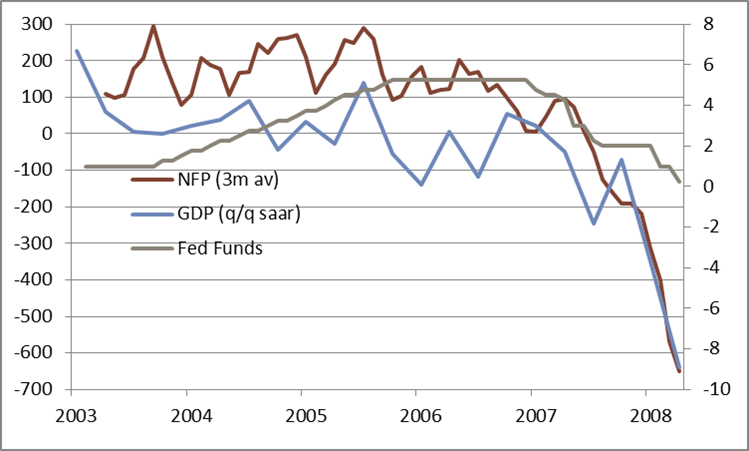

Here is GDP and employment (and Fed Funds) in the period of the last policy tightening that started in mid-2004. This time, rates increased from 1% to 5.25% in 2 years. The start of the process still saw employment growth slow to 100k/m, but GDP growth held up much better - until the end of the move. Then, of course, after the Fed had finished raising rates, everything went very, very badly wrong.

So I will concede that 1994 could have gone better. In particular, If the Fed had worked harder on communication, the markets would have been less surprised when the first rate hike was announced. But, the economy didn't slide back into recession and 1995 to 1999 was simply a very good period for the US economy. This, overall, was no disaster.

The 2004-2006 rate hike cycle by contrast, allowed asset prices to go on rising far too fast, for far too long. Allowed leverage to increase throughout the US and global economies. Again, this is not the place to argue against the general view that the great Crash was mostly caused by greed, and poor regulation. But just as Fed policy caused a slowdown in 1995, Fed policy helped cause a massive recession. So the exit from the last two significant periods of very easy monetary policy both have faults - but are we really supposed to err on the side of a 2004-2006 outcome because we must, at all costs, avoid a repeat of 1994-1995? . But are we that stupid? Employment growth running at 170k/m, and GDP at 2% justify accommodative policy, but not zero rates and massive bond purchases for ever.

The chart below shows US jobs and GDP growth through the 1990s. You can clearly see how in 1994/1995 (when the US Federal Reserve increased its target for Fed Funds from 3% to 6% in 12 months), employment growth slowed from around 350k/month to a trough of around 100k/m, and GDP growth slowed from 5% to 1%. Briefly. Now that is a pretty sharp slowdown and is the basis for arguing that the 'bond crash' represented at the very least a poor piece of policy communication on the Fed's part. Let's forget anything else going on in the world, and accept that if the Fed had either done a better job of preparing financial markets for the necessary monetary policy normalisation, or if they had tightened more slowly, the economy's path would have been smoother.

That's all fine. But what I find surprising is that even now, there is a general sense that the Fed should do everything in its power to avoid a repeat. "We remain unconvinced that the eventual tapering of the central bank's asset purchases will trigger a 1994-style bloodbath in the bond market", John Higgins of Capital Economics is quoted as saying in the Sunday Times today.

The sense that is conveyed is twofold. Firstly, that there is a risk that 'tapering' could be as bad in 2013 or 2014, as raising rates from 3% to 6% was in 1994. And secondly, that the crash was so disastrous everything that can possible be done to avoid a repeat, should be - despite what we have learnt since.

Here is GDP and employment (and Fed Funds) in the period of the last policy tightening that started in mid-2004. This time, rates increased from 1% to 5.25% in 2 years. The start of the process still saw employment growth slow to 100k/m, but GDP growth held up much better - until the end of the move. Then, of course, after the Fed had finished raising rates, everything went very, very badly wrong.

So I will concede that 1994 could have gone better. In particular, If the Fed had worked harder on communication, the markets would have been less surprised when the first rate hike was announced. But, the economy didn't slide back into recession and 1995 to 1999 was simply a very good period for the US economy. This, overall, was no disaster.

The 2004-2006 rate hike cycle by contrast, allowed asset prices to go on rising far too fast, for far too long. Allowed leverage to increase throughout the US and global economies. Again, this is not the place to argue against the general view that the great Crash was mostly caused by greed, and poor regulation. But just as Fed policy caused a slowdown in 1995, Fed policy helped cause a massive recession. So the exit from the last two significant periods of very easy monetary policy both have faults - but are we really supposed to err on the side of a 2004-2006 outcome because we must, at all costs, avoid a repeat of 1994-1995? . But are we that stupid? Employment growth running at 170k/m, and GDP at 2% justify accommodative policy, but not zero rates and massive bond purchases for ever.

Subscribe to:

Posts (Atom)