The speech looks at the role of financial sector drag as a reason for the sluggishness of the economic recovery in many developed economies after the 2008 financial crisis. The BIS view of the world could be summed up as being that equilibrium or natural real interest rates are higher than many policy-makes believe, and this has resulted in an inability to restrain financial booms which cause a misallocation of resources that in turn, leads to painfully slow productivity gains in the subsequent economic recovery.

This is so intuitively true that it needs to be taken seriously. I've reproduced a couple of slides from this presentation and one from an earlier presentation covering the same theme. The first one shows global debt levels rising as a share of GDP, at the same time as real interest rates fall.

If I made the really simple assumption that across the economy as a whole, borrowers pay something like 3% more than the average of the real yields in long-dated government bonds and the central bank policy rate, and that inflation was around 3% in 1986 and 2% in 2015, this chart would suggest that in 1986, overall debt service costs were something like 19% GDP. And in 2015, after almost 30 years of rising debt and falling rates, they were something like 16% GDP. So, no problem then?

You could argue that it makes sense in this world, for policy-makers to accept the downward trend in interest rates. Companies and households alike would and indeed should have more debt because debt-service costs are low. Which is what's happened. Mortgages are bigger as a multiple of income than they used to be (fine if house prices rise for ever, right?) and a glance at the universe of borrowers in the corporate bond market will quickly confirm the gradual downward drift in average credit ratings. A triple-A company with little debt is not maximising the return to shareholders. Better to issue bonds and buy shares back, immediately.

The flaw, is that creditworthiness is a function not solely (or even mainly) of the ability to pay back the interest on a loan. It's about the ability to pay back interest AND principal. In other words, the size of the loan matters. Furthermore, it matters at least as much for the financial sector as for the non-financial sector. If I borrow money from the bank, the bank itself borrows that money too. And if we've learnt nothing else in the last decade, it's that that size of a bank's balance sheet matters. A bank that cares only about keeping income (from interest earned) growing faster than costs (from interest paid) will grow and grow it's balance sheet much as some did in the early 2000s. A focus on return on equity may be Ok for some companies, but not for a bank which needs to care about the return on the capital it uses to earn that money, and needs to set capital aside for the possibility that some of the money it lends never comes back.

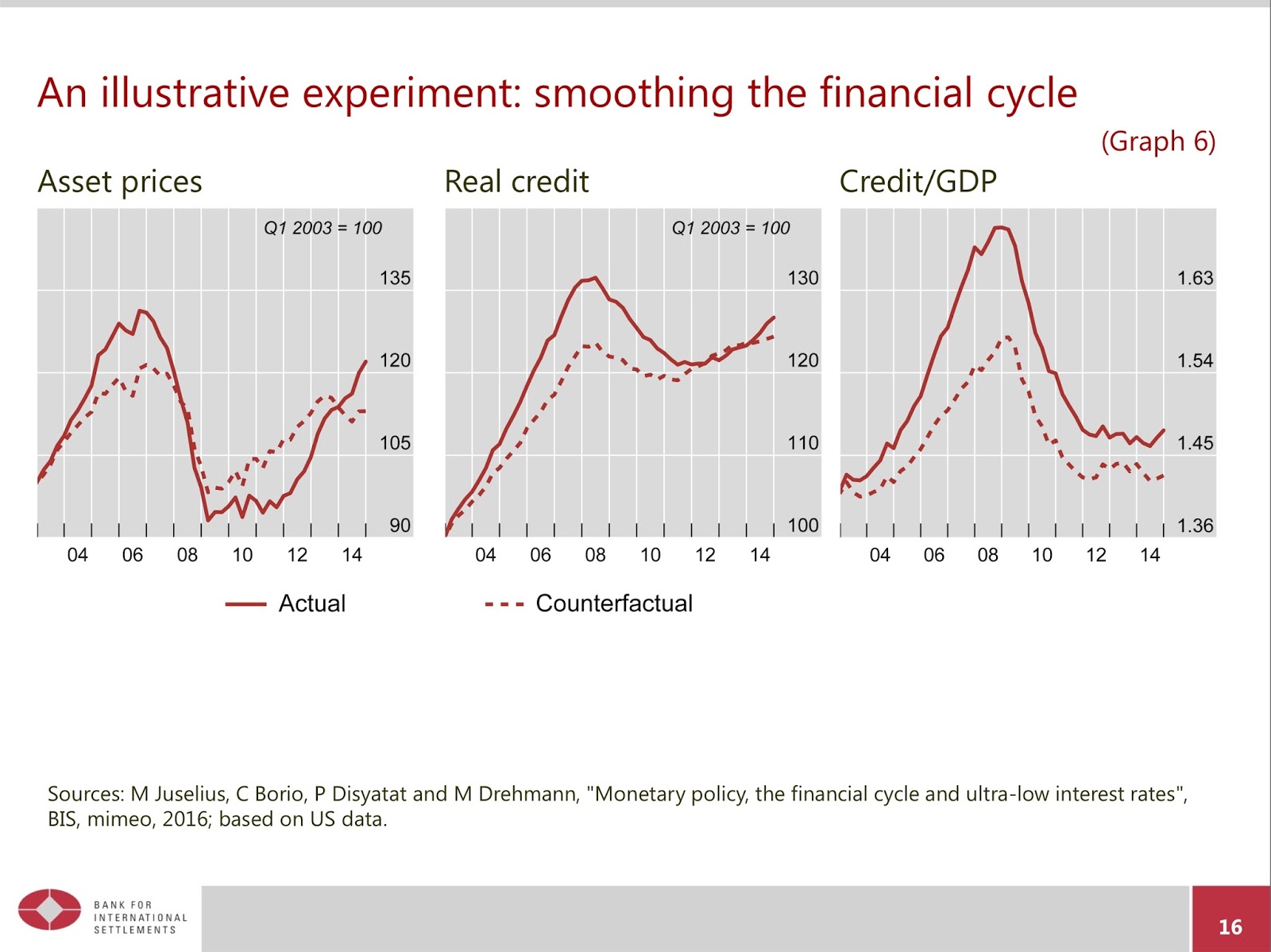

Just accepting that premise implies that the 'equilibrium' which sees more debt and lower rates, is an unstable one. A real equilibrium is one which applies to both the financial cycle and the real economy cycle. As in the second chart I've nicked.....

The crisis followed. Too much money was lent at these low rates. Too many resources were mis-allocated in a world where money was mis-priced. Here's what the BIS' experiment in setting policy to smooth the financial cycle throws out. A cycle, just not nearly such a pronounced one.

After the financial crisis and recession, the misallocation of resources that the financial boom caused/exacerbated, has led to a productivity-free economic recovery, at least in the economies most directly affected. So, estimates of natural rates have come down further. And since there's slack in the global economy, especially if we measure it on the basis of inflation undershooting expectations, policy rates fall even further. The possibility that the inflation cycle is a function of technology and the growth of global markets in goods and labour, is at most only considered in passing.

The depressing thing about this argument, is that the obvious conclusion would be that after a while we're just going to get washed way by another financial boom/bust cycle. Maybe not one whose epicentre is in the US and the UK to quite the same extent as the last one was, but that would be small comfort. It would be better to set global monetary policy with debt levels in mind, before the overall global debt/GDP level gets too much higher.

No comments:

Post a Comment